Offering 1031 Exchangeable Investment Properties

Mulling over whether you want sell your property and not wanting to deal with these issues anymore?

- Rent Control

If you want to switch to from the landlord role to passive investor who has none of the responsibilities and liabilities mentioned above, you could consider investing in high grade commercial properties. Utilizing the 1031 Exchange is a smart way to defer your capital gains tax and transfer your cash to these investments. You can opt to invest into several properties rather than just one.

DST Investments and the 1031 Exchange Process

Delaware Statutory Trust (DST) investments can be suited for the 1031 exchange which defer capital gains and depreciation recapture. DST investments can be purchased at minimum amounts thereby allowing investors to invest in several properties. These investments are typically larger institutional grade properties from retail, healthcare, apartments, and so on with professional management of the property and asset in place to remove investors from the day-to-day operations and management of the property, all whilst receiving monthly cash flow, potential equity appreciation, and tax benefits. One of the advantage of owning shares in a DST is the limited personal liability to the investor: Non-recourse loans and limitations of banks and creditors from going after investors.

Disadvantages of DSTs: There are disadvantages to DSTs including and not limited to:

DSTs are Illiquid—Anyone considering investing into a DST must take into consideration that they are invested until the property is sold.

DST Investors have no control—When the IRS approved the DST structure for 1031 exchanges, it mandated that the 1031 investor could not have any operational control or decision-making authority of the underlying properties.

DSTs Cannot Raise Further Capital—Another IRS mandated tenant. There can be no further contributions or capital raised once the DST has closed to new and current investors. Risks include occupancy rates, major repairs which can deplete cash flow and reserves. It is essential that reserves be set aside for contingencies such as these.

What is a Section 1031 exchange?

Generally, Section 1031 of the Internal Revenue Code of 1986, as amended (the “Code”), provides an alternative strategy for deferring the capital gains tax that may arise from the sale of a property.

By exchanging a relinquished property for “like-kind” real estate, as defined below, property owners may defer their federal taxes and use all of the proceeds for the purchase of replacement property.

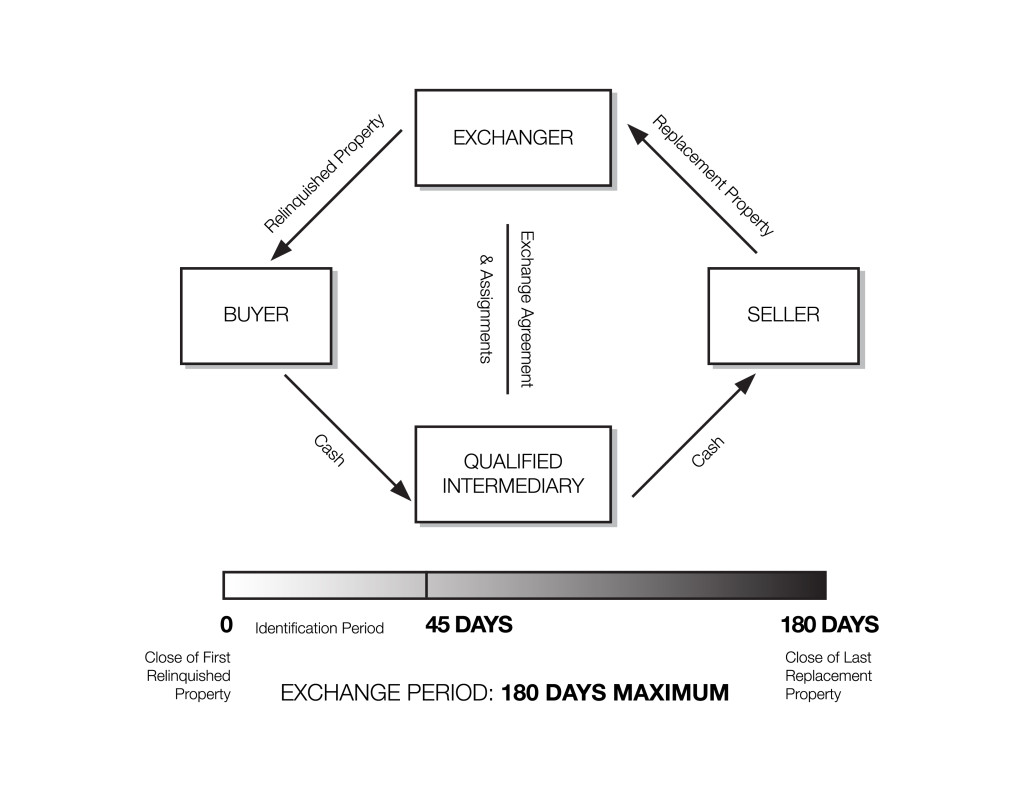

Whether any particular transaction will qualify under Section 1031 depends on the specific facts involved, including, without limitation: the nature and use of the relinquished property and the method of its disposition; the use of a “qualified intermediary” and a qualified exchange escrow, as discussed below; and the lapse of time between the sale of the relinquished property and the identification and acquisition of the replacement property.

What is “like-kind” property?

Set forth below are some examples of “like-kind” real estate:

- Vacant land

- Commercial property, including commercial rental property

- Industrial property

- 30-year or more leasehold interest

- Farm property

- Residential rental property

- Doctor’s own office

- A tenant-in-common ownership interest in an investment property. Tenant-in-common, or “TIC,” ownership is ownership of commercial real estate that has been split into fractional shares. Each owner owns an undivided fee interest in the property equal to his proportionate share of the real estate.

- A beneficial Interest in a Delaware statutory trust, or “DST.” DST interests are described below.

It is important to note that one’s primary residence, as well as vacation or second homes held primarily for personal use, will not qualify for a Section 1031 exchange. However, there are certain safe harbors for vacation and second homes to qualify as either a “relinquished property” or a “replacement property.”

What is a “DST”?

In accordance with the Internal Revenue Service’s Revenue Ruling 2004-86, a beneficial interest in a Delaware statutory trust, or “DST,” that holds a replacement property may be considered “like-kind” replacement property in a Section 1031 exchange. A DST may own one or more properties.

The rights and obligations of investors in a DST will be governed by the DST’s trust agreement. Typically, investors have limited voting rights over the operation and ownership of any properties owned by the DST. In addition, the trustees of the DST may be entitled to certain fees and reimbursements, as set forth in the applicable trust agreement.

What is a “Qualified Intermediary”?

A Qualified Intermediary, or “QI,” is a company that is in the full-time business of facilitating Section 1031 tax-deferred exchanges. The role of a QI is defined in Treasury Regulations. The QI enters into a written agreement with the taxpayer where QI transfers the relinquished property to the buyer, and transfers the replacement property to the taxpayer pursuant to the exchange agreement. The QI holds the proceeds from the sale of the relinquished property in a trust or escrow account in order to ensure the taxpayer never has actual or constructive receipt of the sale proceeds.

A Qualified Intermediary may also be known as an Accommodator, Facilitator or Qualified Escrow Holder.

Certain persons, including those who have acted as the exchanger’s employee, accountant, attorney, investment banker or broker or real estate broker within the two year period preceding the sale of the relinquished property, will be specifically disqualified from acting as a Qualified Intermediary.

What are some key guidelines for a Section 1031 exchange?

- The seller cannot receive or control the net sale proceeds – the proceeds must be deposited with a Qualified Intermediary.

- The replacement property must be “like-kind” to the relinquished property. Both the relinquished and the replacement properties must have been held for investment purposes or for productive use in a trade or business.

- The replacement property must be identified within 45 days from the sale of the original property.

- The replacement property must be acquired within 180 days from the sale of the original property.

- The cash invested in the replacement property must be equal to or greater than the cash received from the sale of the relinquished property.

- The debt placed or assumed on the replacement property must be equal to or greater than the debt received from the relinquished property.

This is a summary of some of the key guidelines for a transaction under Section 1031, but this is not an exhaustive list. The costs associated with a Section 1031 exchange may impact the returns and may outweigh the tax benefits of the transaction. Each prospective investor must consult his or her own tax advisor regarding the qualification of a particular transaction under Section 1031.

How is a property identified for a Section 1031 exchange?

Property identification is done through the Qualified Intermediary. The replacement property must be identified in a written document, known as an “Identification Notice.” The requirements for a property Identification Notice are as follows:

- must include a specific and unambiguous description of the replacement property;

- must be signed by the exchanger;

- for real property, the Identification Notice must include:

- the legal description,

- a street address, or

- a distinguishable name; and

- for property to be produced, such as raw land to be acquired after improvements have been constructed, the Identification Notice should include a description of the underlying real estate and as much detail regarding the improvements as is practical, for example, 100 S. Main St., Anywhere, IL, improved with an 8 unit apartment building.

An identification of replacement property may be revoked prior to the end of the identification period. The revocation must be in writing, signed by the exchanger and delivered to the same person to whom the original Identification Notice was sent. No changes or revocations may be made to the Identification Notice after the end of the identification period (45 days).

The exchanger may identify multiple replacement properties. There are certain additional rules to keep in mind, including the following:

- Three Property Rule: The exchanger may identify any three properties, without regard to their fair market value. The exchanger may acquire one, two or all three of the properties as replacement properties.

- 200% Rule: The exchanger may identify any number of properties, provided the aggregate fair market of all of the identified properties does not exceed 200% of the aggregate fair market value of all of his or her relinquished properties.

- 95% Rule: The exchanger may identify any number of properties, without regard to their value, provided the exchanger acquires 95% of the fair market value of the properties identified.

Are there additional reasons to consider a Section 1031 exchange?

In addition to the objective of deferring capital gains tax, there may be other benefits to participating in a Section 1031 exchange:

- Relieve the burden of active real estate ownership and management

- Exchange a non-cash flow producing property for a cash flow producing property

- Diversify into a portfolio of properties

- Diversify an existing portfolio by geography and property type

- Obtain ownership in higher-grade commercial properties

- Facilitate estate planning

Do vacation and second homes qualify for Section 1031 exchanges?

Vacation or second homes held by the exchanger primarily for personal use do not qualify for tax deferred exchange treatment under Section 1031.

The safe harbor for a vacation or second home to qualify as relinquished property in a Section 1031 exchange requires the exchanger to have owned the property for twenty-four months immediately before the exchange, and within each of those two twelve-month periods the exchanger must have:

- rented the property at fair market rental for fourteen or more days, and

- restricted personal use to the greater of fourteen days or 10% of the number of days that it was rented at fair market rental within that twelve-month period.

For these purposes, “personal use” includes use by the exchanger’s friends and family members that do not pay fair market value rent.

Are there vesting issues to consider in a Section 1031 exchange?

Yes. For an exchange to satisfy Section 1031, the taxpayer that will hold the title to the replacement property must be the same taxpayer that held title to the relinquished property. However, business considerations, liability issues, and lender requirements may make it difficult for the exchanger to keep the same vesting on the replacement property. Exchangers must anticipate these vesting issues as part of their advanced planning for the exchange.

There are some exceptions to this rule when dealing with entities that are disregarded for federal income tax purposes. For example, the following changes in vesting usually do not destroy the integrity of the exchange:

- The exchanger’s revocable living trust or other grantor trust may acquire a replacement property in the name of the exchanger individually, as long as the trust entity is disregarded for federal tax purposes.

- The exchanger’s estate may complete the exchange after the exchanger dies following the close of the sale of relinquished property.

- The exchanger may sell a relinquished property held individually and acquire a replacement property titled in a single-member LLC or acquire multiple replacement properties in different single-member LLCs as long as the exchanger is the sole member and the single member LLCs are treated as disregarded entities.

- A husband and wife may exchange a relinquished property held individually as community property for a replacement property titled in a two-member LLC in which the husband’s and wife’s ownership is community property, but only in community property states and only if they treat the LLC as a disregarded entity.

As a general rule, the exchanger should not make any changes in the vesting of the relinquished or replacement properties prior to or during the exchange. Exchangers are cautioned to consult with their tax or legal advisors regarding how their vesting issues will impact the structure of their exchange before they transfer a relinquished property.

What is a Section 1033 exchange?

Section 1033 of the Code covers “involuntary conversions,” including natural disasters and losses via eminent domain. Property owners may not realize that funds received as a result of these actions – condemnation award proceeds or insurance proceeds – would normally trigger recognition of gain. Section 1033 of the code, similar to Section 1031, allows taxpayers to defer that recognition of gain.

While similar to a Section 1031 exchange, Section 1033 has some notable differences:

- There is no concern about the taxpayer’s “constructive receipt of funds;” therefore there is no need for a qualified intermediary.

- Taxpayers have a longer period of time to identify replacement property and reinvest proceeds – generally up to two years, and even up to three years or longer in certain circumstances, such as involuntary conversions arising from certain federally declared disasters.

Important Notes

The information contained herein is neither an offer to sell, nor the solicitation of an offer to buy any security in any program sponsored by Inland Private Capital Corporation, which can be made only by the investment-specific Private Placement Memorandum, and sold only by broker dealers authorized to do so. Any representation to the contrary is unlawful.

The information contained herein is a brief and general description of certain guidelines regarding Section 1031 exchanges. All prospective investors should consult with their own tax advisors regarding an investment in a program sponsored by Inland Private Capital Corporation.

Consult With Legal, Financial and Tax Advisors

You should always consult with your legal, tax and financial advisors prior to entering into any 1031 Exchange or Delaware Statutory Trust or DST investment property transaction, including the review of any Private Placement Memorandums (PPMs) or other offering material on Delaware Statutory Trusts or DST investment property interests.

Comments are closed.